Navy Federal, About Black Mortgage Applicants?

What's behind the 50% denial rate for black home mortgage applicants?

Modern-day redlining? Maybe, maybe not. I came across a CNN story on the denial rate of black mortgage loan applicants at Navy Federal Credit Union: They are the largest credit union in the country, with $156 billion in assets. They denied 52% of black applicants, compared to 33% of white applicants. Full disclosure: I am a member; thanks, Mom and Dad. They denied the subject of the story due to “excessive obligations about income.” The debt-to income ratio is an underwriting factor in your loan's suitability. If it is too high, you may get denied. For instance, for a conventional FHA loan, the mortgage portion of your debt should not exceed 31% of your monthly debt obligations, and all obligations should not exceed 43%.

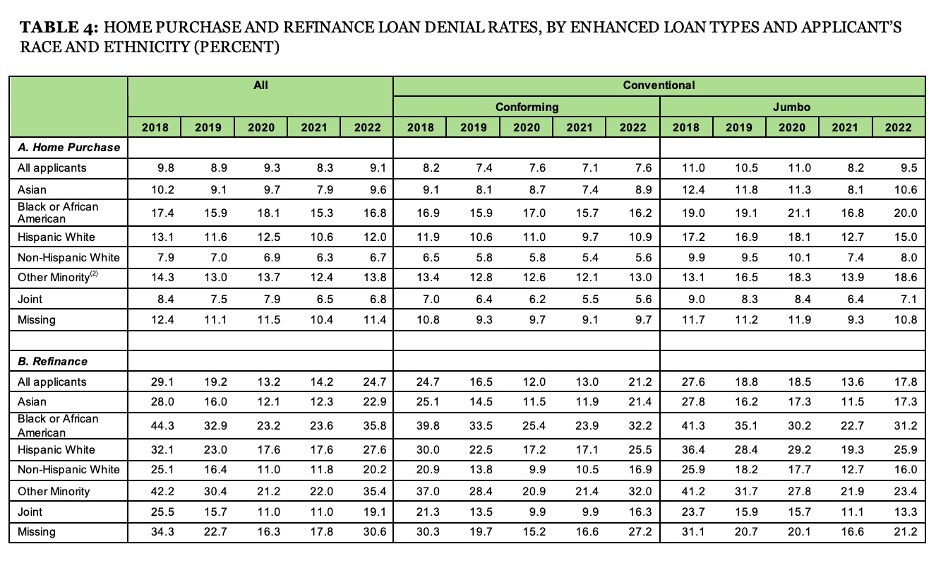

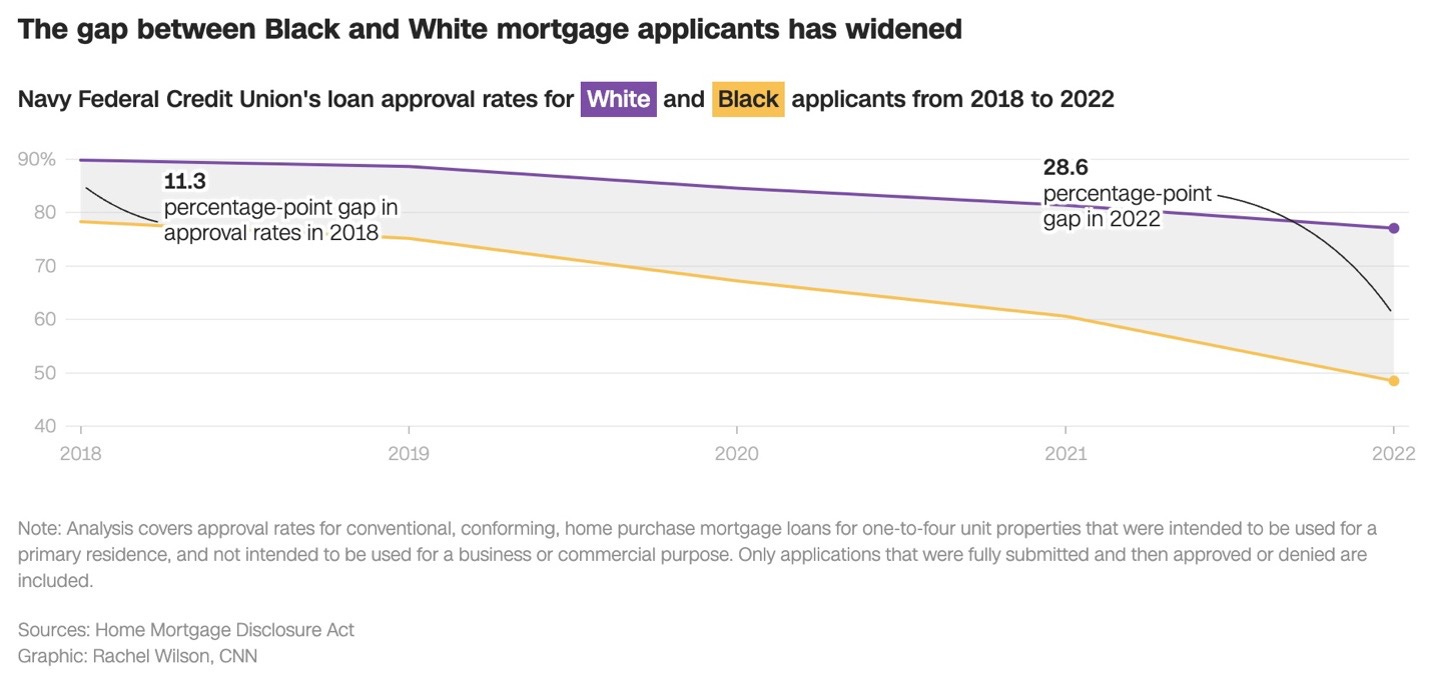

There is no concrete explanation, but considering the data points, the optics look skewed towards racial discrimination. Going to the source data, which was the Data Point: 2022 Mortgage Market Activity and Trends (see table 4) Navy Federal has a rejection rate for black applicants that is three times the national average for conventional conforming loans. That decline rate has been increasing over the years (see table 5 CNN graphic below). There are a myriad of factors at play, from automated underwriting to allowing applications that may not have any shot at final approval.

‘Financial literacy is not a panacea’

I ran a small boutique mortgage brokerage company in the late mid- to late 2000s, up to and through the meltdown. Think about the movie The Big Short, it was that era of housing loans. Being a licensed mortgage broker, I did observe a trend in the number of black customers who came to me for a second opinion after their banks rejected them. Truth be told, this is a complicated issue because even when using four common factors as a control group (income, debt, property value, and down payment), other issues may arise. Creditworthiness stands out as a potential cause for higher rejection. A 2021 study by Shift showed an average credit score by race: Asian (745), White (734), Other (732), Hispanic (701), and Black (677).

Another is the obligatory nature of being a minority and their monetary responsibility to their extended family. According to Pew Research, “Black households were significantly more likely to assist those outside their immediate family (35 percent) than were white (25 percent), Hispanic (24 percent), or other households (27 percent).” This can be a hidden factor because it may not show up on a credit report unless asked directly. It can still affect your ability to repay a loan, even if it is not a defined debt obligation. Financial literacy is not a panacea and may not solve the racial rejection problem in the mortgage and banking industries.

Here are a few tips to avoid denial:

Navy Federal has two types of pre-qualifications. 1) a pre-approval letter that does not require any documents up front, and 2) a verified pre-approval letter that allows you to qualify for a mortgage rate lock after you provide your documented financial information. Widespread implementation of the latter may lead to fewer rejected loans for all applicants.

o Familiarize yourself with the 1003 form before applying for a loan. This is the Uniform Residential Loan Application form that you will fill out when you purchase a home. Just a note, section 10 has the demographic information for government recording purposes.

o Know your credit score ahead of time. Most lenders will use your Fico 8 score, which you can get from Fico.com.

o Applying for a mortgage loan will be a hard pull, which will lower your score. However, the free scores that are available may or may not align perfectly with the score they used to qualify.

o Once a credit check is done on you, try to avoid new inquiries. Any drop in your score may affect your approval odds or interest rate.

o Do not increase your debt load. Your debt-to-income (DTI) ratio will determine the amount of money a lender will approve you for. For an FHA loan, your debt-to-income ratio should not exceed 43% total and 31% for the mortgage.

o Do not switch jobs between the initial application and loan closing. Staying within the same field may be acceptable, but it will trigger a new set of verifications and may affect your loan.

Finally, work with someone you feel comfortable with. There are a lot of mortgage products available, and you need to make sure that you understand and can afford them. Consider a first-time homebuyer class as a primer or a refresher if you are new to home ownership.

Table 4

Table 5

In the interest of fairness here is the generic lackluster response from Navy Federal:

“Navy Federal Credit Union is committed to equal and equitable lending practices and strict adherence to all fair lending laws. Employee training, fair lending statistical testing, third-party evaluations, and compliance reviews are embedded in our lending practices to ensure fairness across the board. CNN’s recent analysis of mortgage lending data does not accurately reflect our practices, and furthermore their mortgage data model does not account for major criteria required by any financial institution to approve a mortgage loan.

As a not for profit, member centric, membership organization, we are focused on expanding awareness and access to homeownership across the country. We are proud of the fact that we provide a higher percentage of mortgage loans to Black applicants than the vast majority of the top 50 mortgage originators nationwide.

Navy Federal has more than 350 branches worldwide with over half of our stateside branches located in minority communities. In addition, we hosted over 600 home-buying education seminars nationwide this year. Navy Federal is a trusted financial partner for all its members and advises each member based on their unique financial needs.”

Navy Federal Credit Union Spokesperson

More thoughts, stories, and articles will be published on the “Introducing Money One Word at a Time” Substack column of Jason Taitt. You can subscribe here.